a)

A summary of my returns versus the indices

b)

A review of my investing strategy and what can be

improved on

c)

Observation of the market

d)

A short summary of the “bad news” this year and my

opinions on it.

Vanguard S&P 500 ETF

Start of Year: 247.09

Today: 227.76

Dividends: 8.062

Returns: (227.76+8.062)/247.09 = -4.56%

SPDR STI Index Fund

Start of Year: 3.48

Today: 3.1

Dividends: 0.113

Returns: (3.1+0.113)/3.48 = -7.67%

Tracker Fund of HK

Start of Year: 30.05

Today: 25.65

Dividends: 0.95

Total return: (25.65+0.95)/30.05 = -11.48%

Personal: 4.15%

Compared YOY, dividend payments

increased slightly due to increased capital injection. Yield has increased

slightly, but at this stage, dividend investing is not my main concern.

I glad to have 4.15%; it feels a tad

disappointing to have lost a 20+% lead over the indices to 11%-15%. Looking

forward, if I could seriously have a 10% lead over the indices, I probably make

so much money that I wouldn’t care. But there is no way to tell.

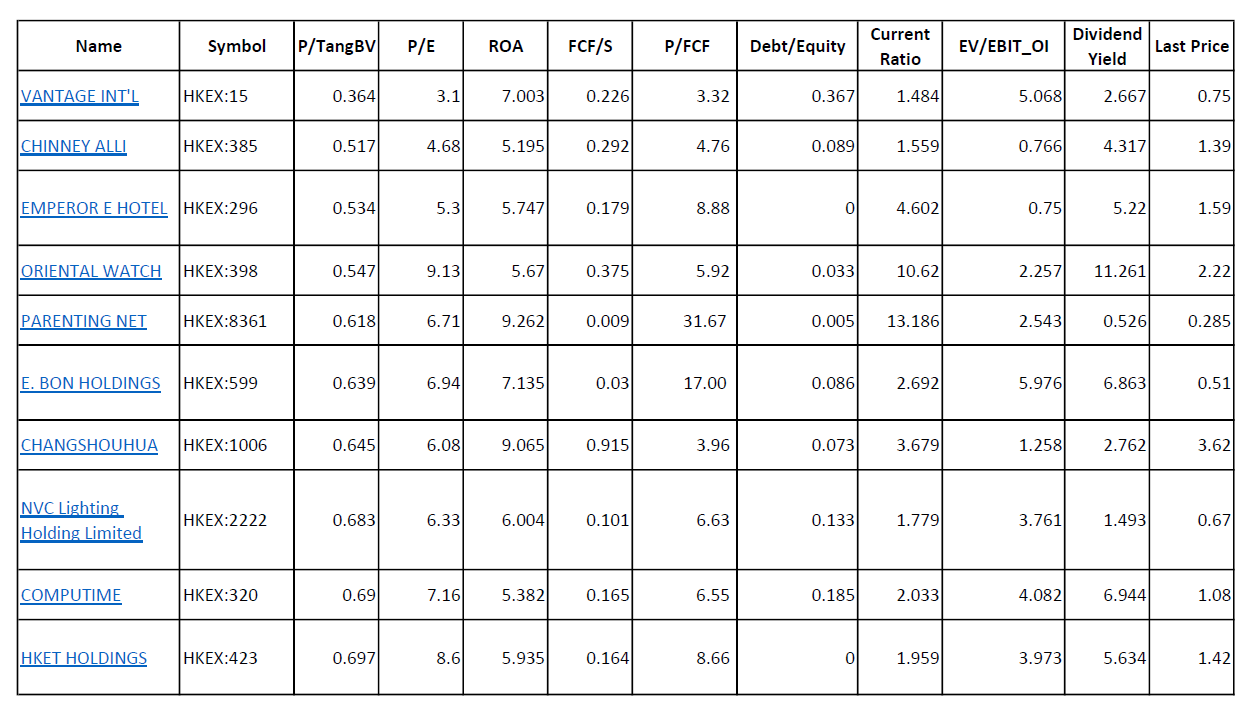

Investing Strategy

My approach is to look for easy

deals, i.e. no brainers. A simple idea takes no more than a paragraph or two to

describe.

***

A word about “easy.” What exactly is

easy? Let me illustrate:

Imagine a hypothetical company that

makes toilet brushes. Revenue and bottom line has been stalling or suffering

slight dips for the past four years. Net margins has never dip below 30% for

the last 9 years. Every year, its net operating cashflow has been over 100m, and capital

expenditure has been only 3 to 5 million for the last ten years.

Insiders has been buying stock. But

the market, in all its collective wisdom values it at 7.7 price to earnings

(PE). Market capitalization stands at 1.14B.

Given that it has a cash hoard of

over 271m and no debts, the company is actually selling for 869m. That means the company is priced at less than

9 times free cash flow.

A casual market observer will point

out that we are in volatile times. Tariffs are imposed between two of the

world’s superpowers. Nobody is certain what would happen in the near future.

But this company does not derive a sizeable revenue overseas.

The overseas opportunities for this

company looks uncertain, but the risk in terms of valuation is

low.

Would you be buying more stock if

the market decides to slash its asking price by 20%? I certainly will!

***

The best companies to buy are

companies with problems, but possessed a wonderful track record, with decent

management and dividends to boot.

The former boost your chances of recovery,

the latter pays you for waiting. The lovely thing about problems is that usually

companies will overcome it, and an investor might be able to assess the

probability of that success with some experience. With problems come

uncertainty and risk. I cannot account for uncertainty, but accounting for

risk, as defined by difference in value versus market pricing, is my job.

Since market is usually efficient, good

deals are usually scarce. I aim to avoid over diversification; having more than

8 or 9 stocks is a crowd.

What I could improved on, was the

amount of transactions made. Transaction cost is reduced from 0.65% to 0.55%

this year, but the number of transactions is 59 vs 54 and 58 the previous two

years. I hope to do better than this next year. The interesting figures are how

many buys vs sells executed in each of those years.

Year

|

Buys

|

Sells

|

Market

Returns*

|

2018

|

39

|

20

|

-7.14%

|

2017

|

31

|

23

|

21.11%

|

2016

|

44

|

14

|

5.03%

|

* SPDR Straits Times ETF (es3)

figures from Stocks.Cafe.

In terms of absolute dollars, I was

a net buyer in 2018 and 2016, and a net seller in 2017. On hindsight, maybe it

is a good thing since the indices are returning negative this year, where one

should be a buyer?

The other lacking effort on my part this year

is the absence of quality special situations investing this year. The Religare

Health Trust (RHT) sale to Fortis wasn’t very well researched, and even with

the information I knew that time, the deal felt like a “50-50,” where the odds

were simply not great. I was lucky to exit the position with small profits.

TBH, I have never seen a deal with so many twist and turns like RHT. It takes a

lot of courage to hold on.

A lack of discipline was also

invested in other “50-50” deals which was subsequently sold at a

small loss/profits. This is disappointing as the lack of discipline will only

result in a huge losses in the long run. Lesson learnt—only initiate a position

when I am willing to put in 10% or more of my net worth into it.

Observations about the market

The number of going-private deals

declined since the start of this year. I believe that a rising number of

going-private deals indicate a cheap market. I will be keenly reading the news

on any trends of such. The dearth of IPOs is another murky indicator too,

although the quality of IPOs coming to SGX is usually poor..

The idea of buying the dips was popular

earlier this year… but all it took was December to vanquish it. Quick rebounds

returns simply halted.

Just for the sake of entertainment,

I reviewed the chart of 2018, Vanguard S&P 500 ETF, and counted the amount

of dips and peaks in which an incredible trader could participate in.

An impossible 51% gain awaits any

trader who, unrealistically I must add, is able to participate in every dips

and recovery. Such a miraculous operation is quite impossible, since it requires

god-like timing. The above trades did not include the deadly December

correction.

What happens if this trader refuse

to stop and carried on till December?

He would have exited 33.9% richer have he sold on Christmas Eve, and 41.8% if sold just 3 trading days later. Huge difference.

Trading, such an exciting game.

These small, single-digit gains were no results of intelligence but out

of bravado. How can such a method be reliably used? Nobody has an idea what

tomorrow brings. The only endearing fact, which decades of financial academia

has proved, is that equities will return more than bonds in the long run. The

long run is 10-20 years and not 10-20 days periods that buying on the dip

entails.

The market is a tough, mean bastard and there must be a source which participants obtain their mental fortitude from.

Buying the Bad News

There were plenty this year. Some

that I could recall:

- Comfortdelgro “recovering” after the Grab/Uber deal and its decline after the arrival of Go-Jek

- SingTel and its troubles in Indonesia and India

- Kimly-Asian Story-Pokka deal which got the latter’s CEO suspended and Kimly directors’ passports impounded.

- Lippo Group-Meikarta senior executives arrest and the subsequent sell-down of all its listed subsidiaries before and after the news

- Litigation in Top Glove following an acquisition

- Malaysia “Freak” Election results

- The loss of a major customer for Serial Systems (almost a 50% sell down)

- The Datapulse Tech fiasco

Personally, I love bad news. But I

have my own opinions on this.

I think one should avoid buying the

“bad news” on two situations.

1) When the

integrity of the owner/managements is suspect. Who is

responsible for producing the financial statements that we as investors rely

on? There are hundred and one ways for management to profit, but only one way

for small retail investors like us.

2) Avoid

companies who can’t compete with the low-cost competitor. Nobody could

beat Nebraska Furniture Mall with a ferocious Mrs. B. As long as the low-cost

competitor is profitable, this is going to be a long term problem. Likewise on a long-term basis, there can be no way a rationale consumer will choose

something that cost more.

Graham has a point when big enterprises

hit a bad patch, the odds of them overcoming it is good due to the resources

(but human and capital) they have. However, I do feel that we had a huge bull

run—most equities are priced on the high side. As such, these troubled,

unpopular companies are unlikely to be priced at a bargain. There is no substitution

for valuation.

Do not expect the market to be kind-- only wish that it will become sane in the long run. I wish everyone good health.